Three stocks to watch as housebuilders strengthen foundations

In his FTSE Sector Watch column, Richard Hunter explains how several tailwinds have left the housebuilde…

3rd March 2020 10:26

by Richard Hunter from interactive investor

Share on

In his FTSE Sector Watch column, Richard Hunter explains how several tailwinds have left the housebuilders in a strong position.

This piece was written before the coronavirus severely impacted markets.

The housebuilders have at different times found themselves on a sticky wicket this century, but as a rule, they have weathered the storm.

As defined by the London Stock Exchange (we are limiting the scope of this article to the FTSE 100), the Household Goods and Home Construction sector is comprised as follows:

Barratt Developments is engaged in acquiring and developing land, planning, designing and constructing residential property developments and selling the homes it builds throughout Britain. The company operates in two segments, Housebuilding and Commercial developments, the latter of which is delivered by Wilson Bowden developments.

- Invest with ii: Top UK Shares | Share Prices Today | Open a Trading Account

Berkeley Group through its subsidiaries is engaged in the residential-led property development, focusing on urban regeneration and mixed-use developments in London and the South of England.

Persimmon through its subsidiaries is engaged in the housebuilding business, trading under the brand names of Persimmon Homes, Charles Church, Westbury Partnerships and Space4. Its Space4 business manufactures highly insulated timber frames, wall panels and roof cassettes.

Taylor Wimpey offers homes from apartments to five-bedroom houses. In 2007, George Wimpey and Taylor Woodrow merged to form Taylor Wimpey. It now operates from 24 regional offices across the UK, along with a small operation in Spain, where it builds homes in various locations of Costa Blanca, Costa del Sol and the island of Mallorca.

Difficult past

Leading up to and during the financial crisis, some housebuilders found themselves with excess land that was going to be difficult to sell; there was a series of governmental and party positions on how property should be taxed; and the referendum of 2016 saw the sector’s share prices plummet on fears of ongoing weakness in the UK economy.

However, there has been a recovery in the sector’s fortunes driven by several tailwinds which have left the housebuilders in a strong position.

For example, the government’s Help to Buy scheme, launched in 2013, buoyed prices and helped to transform company profit margins over the decade, with the resulting build-up of surplus capital benefiting shareholders in the form of annual and special dividends in abundance. In addition, historically low interest rates, few problems surrounding mortgage availability and a general housing supply shortage have all played into the sector’s hands.

More recently, the removal of a layer of political uncertainty after last year’s general election, plus the past year which saw the UK housing market showing signs of stability despite political and economic headwinds, have also contributed to this cyclical sector dominating the decade for FTSE 100 index stocks.

This has been achieved during a time when the UK banks and housebuilders found themselves squarely in the Brexit firing-line amid uncertainty around both whether it would even happen and, if it did, what the economic impact might be to the UK.

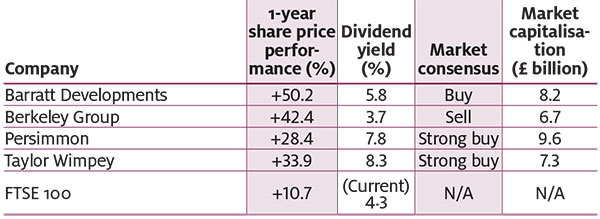

Tale of the tape

Note: Because of the proliferation of special dividends in the sector, the above table shows projected yields (rather than current, which only takes ordinary dividends into account). Sources: 27 January 2020: Digital Look/ProQuote/FT

End of Help to Buy

Further out, the removal of the Help to Buy scheme is on the distant horizon and currently planned for 2023 – its removal will no doubt punch a large hole in profits, and the sector as a whole will need to take action to replace them. Moreover, the cyclical nature of the sector means it would of course be hit by lower consumer confidence or higher interest rates.

Challenges remain, but for the most part these companies are in a much stronger position than they were leading up to the financial crisis, and the financial steps they have taken since leave them ready to fact the next exogenous crisis, whatever that might be.

Three stocks to watch

Barratt Developments: at the company’s full-year results in September, Barratt showed that solid financial foundations remained in evidence. Net cash, although slightly down on the previous year, still stood at £766 million, enabling the payment of a generous dividend. Meanwhile, the company retained the right to switch between share buybacks and increased dividend payments.

Elsewhere within the numbers, there were strong signs of progress – pre-tax profit increased by 9% to a figure bang in line with previous guidance, basic earnings per share rose 10%, operating margin was a healthy 19% and the return on capital figure of 30% was impressive. At the same time, the outlook was favourable, with Barratts managing its highest number of completions since the financial crisis, and with total forward sales looking strong.

Like the UK economy itself, the shares of the company have been resilient and have made some progress, although it can only be a matter of conjecture as to how much stronger this could have been.

Persimmon: has recently suffered from difficulties of its own making, with its quality issues in terms of both build and customer service widely reported and criticised. The company has put these matters at the top of its “to do” list and there has been an inevitable impact on sales in the intervening period.

Even so, there remains much in Persimmon’s favour. It has a deep landbank and is determined not to repeat the mistakes made leading up to and during the financial crisis, such that the company is now the proud owner of a strong balance sheet, with a particularly cash-generative business. The group’s payment of lofty special dividends in recent times has led to a projected dividend yield of over 8%. Meanwhile, despite the shaved revenues reported in its latest update, Persimmon maintains that pre-tax profits will not suffer and will continue to be in line. The imminence of the spring selling season should provide another fillip to progress.

Taylor Wimpey: Taylor Wimpey had previously left itself much to do in the second half of the year to get back on track, which seemed to have been achieved after its recent update. A record order book of around £2.2 billion represented an increase year-on-year of 22%, while the operating profit margin of 19.6% was perfectly adequate. Meanwhile, the net cash balance was £546 million, and Taylor Wimpey’s long landbank also offered solace, with the current figure stable at 76,000 plots and the strategic pipeline at 140,000 potential plots.

Naturally concerns remain, such as at the higher end of the housing market, where there has been some pressure, particularly in London and the South East to which Taylor Wimpey is exposed. In 2020, the company’s performance will likely be second-half weighted, while there may be some headwinds developing with the Europe negotiations.

Richard Hunter is head of markets at interactive investor, Money Observer’s parent company.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.