Troy’s Francis Brooke: how I’m repositioning my income funds for tougher times

Troy Trojan Income manager cautions the fund's stellar run in growing its dividend is likely to come to …

4th September 2019 11:23

by Kyle Caldwell from interactive investor

Share on

Troy Trojan Income manager cautions the fund's stellar run in growing its dividend is likely to come to an end in 2019, and has been busy making changes to the portfolio to reduce risk.

There are plenty of funds with the word ‘income’ in their name; but out of a pool of 58 open-ended UK equity income funds, just two have delivered consistent annual growth in their income over the past decade, research by analyst FundExpert found earlier this year.

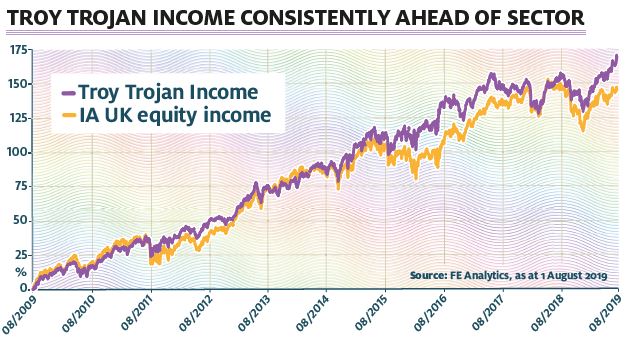

One of the funds that have delivered on this front is Troy Trojan Income, which has been managed by Francis Brooke since launch at the end of September 2004, nearly 15 years ago. Over this period the fund’s dividend has grown by 4.9% on average each year, but Brooke is keen to stress instead the inflation-adjusted figure of 1.9%. Total returns have also impressed: the fund has comfortably outstripped the benchmark FTSE All-Share index, returning 182% against the index’s 151% over the 10 years to end July 2019.

It is a similar story for the Troy Income & Growth Trust (TIGT), a Money Observer Rated Fund and mirror version of the open-ended fund, which has been managed by Brooke since he took over at the end of July 2009.

But Brooke has cautioned that the stellar run in growing the Troy Trojan Income fund’s dividend is quite likely to come to an end in 2019, and has been busy making changes to the portfolio to reduce risk. Brooke notes: “The current market conditions represent too great a risk to capital.”

He acknowledges it is therefore “quite likely that the final dividend will be slightly lower than in the previous year”. Unlike Troy Income & Growth Trust, the open-ended fund does not have revenue reserves to draw on.

A more defensive gear

The move to shift the portfolio into a more defensive gear has not been influenced by macro unknowns such as how Brexit will pan out, but was instead borne out of the current state of the UK dividend market. Although income payments are expected to hit a record high in 2019, surpassing £100 billion for the first time, Brooke points out that there is a high number of shares with yields higher than the average for the market as a whole – a sign that some firms seem to be overstretching themselves to keep income investors sweet, or that the market expects dividend cuts down the line.

“There’s a big split between the high- and low-yielding shares. There’s not that much choice in the middle – a real shortage of businesses yielding between 4% and 5%,” says Brooke. He describes this as an “awkward situation,” and feels it is a prudent time to reduce risk and “improve the quality of the portfolio to have less emphasis towards this part of the market”. He adds: “We have been putting money into shares that we feel more comfortable in. We are re-booting the income growth engine of the Troy Trojan Income portfolio.”

- What will Boris Johnson do for your money?

In turn, he cautions that by reducing emphasis on the high-yielding part of the market there is likely to be “pressure on the income account” of the fund over the next couple of years. In contrast, TIGT is better-placed, with nearly three quarters of a year’s income in its dividend reserves.

Focus on consistent delivery

It is a refreshingly honest assessment, given that most fund managers tend to talk up their own book. “As we have been making some adjustments, I do expect dividend growth to be slower in the short term. But we want to ensure the businesses we hold in the portfolios can consistently deliver across the entire business cycle. And such business are typically yielding between 3% and 4%, but they are generating enough cash to pay dividends, rather than overdistributing and potentially hampering their long-term growth prospects.”

One of the key moves to reduce risk has involved a shift away from utilities, selling Severn Trent and Pennon and more recently reducing exposure to Centrica, the owner of British Gas. “The political and regulatory backdrop has dampened the appeal,” he says; for similar reasons Royal Mail has also been sent packing.

The proceeds have been put to work in lower-yielding names that Brooke views as being more dependable dividend payers. One new holding is Associated British Foods, which counts Primark as one of the many brands it owns. Another new position has been built in Victrex, which manufactures a polymer used in cars, aeroplanes, mobile phones and even Dyson vacuum cleaners. The structural advantage of the business, says Brooke, is down to the exacting manufacturing involved in processing the material. “Its patent expired in the 1990s, but the company still boasts 70% of global production. Other businesses have generally been reluctant to challenge Victrex’s dominance,” he adds.

Both the fund and the trust look for shares with three indicators of quality. The first is pricing power, found for example in businesses that are providing essential products or services. The second hallmark of quality involves barriers to entry such as intellectual property that cannot be replicated by rivals. Thirdly, Brooke looks at the structure of certain industries as another way to find shares that tick the quality growth box; he gives the example of those with high switching costs.

- Three months after the suspension, how is Woodford Equity Income getting on?

Once all these quality ingredients are put together, Brooke looks to strike a balance between capital and income, with a focus on preservation of capital. He adds: “To achieve this, the portfolios are populated with businesses with a higher- than-average propensity to generate higher-than-average free cash flow.”

Consumer goods businesses are by far the biggest sector bet, accounting for just over a quarter of both portfolios. Brooke acknowledges that valuations are high compared to history for the likes of Unilever et al, but when taking a step back and looking at today’s valuations in context with their price-to-earnings ratio range over the past five years, the price tags begin to look more reasonable. Some international shares are also held in this segment of the Troy Trojan Income portfolio, including Nestlé and Procter & Gamble.

Overseas revenues

Overall, around 70% of the fund’s underlying revenues are generated overseas. Some domestically focused businesses are held, but Brooke has not joined the growing crowd of UK fund managers increasing exposure to this area on valuation grounds. Three domestic shares he does like, though, are Lloyds Banking Group, Next and Domino’s Pizza.

At the latter stages of what most regard as a bull market looking long in the tooth, Brooke is seeking to get the portfolios in order for potentially tougher times to come. Performance-wise, both last year and following the Brexit vote in June 2016, the portfolios suffered knocks as economically sensitive shares shone. These included miners and housebuilders, two sectors Brooke says he “does not play in”.

But over the long run the portfolios have impressed and rewarded the strong following they have built up through the years. A decade ago both had £50 million of assets under management, but today Troy Trojan Income has £3 billion and TIGT £240 million.

Brooke concludes: “We do not want to make a macro bet on the UK economy and have relatively little exposure overall. In regard to the macro, we have no idea what will happen to Brexit or other things such as the US/China trade war or what Donald Trump will do. But what we do have control over is ensuring the portfolios do the job our investors want them to do.”

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.