How to invest a pension for a regular income: three common retirement scenarios

We outline flexible solutions for a sustainable, reliable income from your pension in three different sc…

12th March 2020 11:29

by Kyle Caldwell from interactive investor

Share on

We outline flexible solutions for a sustainable, reliable income from your pension in three different scenarios.

For those at retirement who choose to take advantage of the pension freedoms introduced in 2015, the key attraction of this option is likely to be its flexibility. By opting to leave your pension invested, there is scope for capital to grow, income is generated and on your death any unused capital can be passed on to your family.

The alternative – which, for most people in an investment pot-style (defined contribution) pension, was the only option prior to 2015 – is to use your pension to buy an annuity, which provides a set level of income for the rest of your days. The big trade-off is that your capital is forfeited.

Undoubtedly, for many people the flexibility of ‘pension freedom’ solutions outweighs the security annuities offer. As a result, there has been a notable increase in retirees investing their pension pots to generate income, despite the fact that annuities, although no longer the draw they were a couple of decades ago, are still not easy to beat.

- Learn more: How SIPPs Work | SIPP Portfolio Ideas | Open a SIPP

According to Hargreaves Lansdown data, in 2003 a healthy 65-year-old would have seen £100,000 purchase an annual income for life of £7,337. Today, annuity rates are less generous, because of increasing life expectancies (which means pension capital needs to provide more years of income) and the fact that interest rates are at rock-bottom (which means returns on capital are lower). The same £100,000 would yield around £5,000, or 5%.

This is not to be sniffed at: certainly, a reliable 5% return from investments year in, year out is unrealistic given the ebb and flow of stock markets. Financial advisers and planners face this dilemma every day. So can the stock market deliver a better outcome than an annuity?

- Retirement guidance: coming soon to a pension provider near you

- How to trim tax on pension pot withdrawals

- What not to do with your pension

- 11 investment trusts for a £10,000 annual income

- Steve Webb: the biggest pension freedom trap to avoid

Tailored solutions

No single plan will suit everyone, as personal circumstances vary. However, following conversations with financial planners, Money Observer has come up with solutions to meet three common goals among people who want to take advantage of the pension freedoms to generate monthly income from their investments.

Where relevant, we explain the investment mix that would be required – and offer a reality check.

1) I want a higher level of income than an annuity offers, but to maintain my capital

The aforementioned 5% target is not easy to generate as a natural income yield. Gavin Haynes, an investment consultant at Fairview Investing, describes it as “demanding”, given that a balanced portfolio consisting of an equal split of equities and bonds would yield more in the region of 3.5%-4%. He says: “You would have to look at emerging market debt funds and income funds that pay an enhanced level of income by sacrificing capital growth. These offer some of the most attractive yields, but are at the higher end of the risk spectrum.”

Combined strategy

Further risk arises from focusing purely on yield. According to Rosie Bullard, a portfolio manager at James Hambro & Partners, this used to be a routine approach, but because of what has happened to interest rates and bond yields over the past decade, it is no longer a given. She says: “These days retirement income is usually best taken from a combination of dividend income and capital growth. Going for high-yielding companies because you want a high level of income is not an effective strategy.”

Instead, the overriding message is to reduce risk by aiming to generate a lower level of income and then sell down capital to achieve a 5%-plus total return.

Patrick Connolly, an independent financial adviser at Chase de Vere, says: “It was previously considered possible to hold a balanced and diversified investment portfolio – including equities, fixed interest, property and cash – to generate a natural income of around 5% a year, and still achieve some capital growth. But in the current climate, a monthly income of 3%-4% is a much more sensible target.”

Connolly recommends UK equity income and global equity income funds for the core of a pension portfolio of this type, alongside a range of fixed-interest assets that will provide an income but should also offer additional stability in a portfolio if stock markets suffer a prolonged downward spiral.

It’s worth noting that individual circumstances will dictate whether investors are in a weak or strong position to achieve a total return in the same ballpark as an annuity total return.

For instance, someone who has a final salary pension and other investments such as Isas to draw on has more options available to cover basic living costs (alongside the state pension), so they can afford to take the additional risk entailed in generating an income when they retire.

Connolly says: “Those with just a pension fund should consider buying an annuity with part of it. This will give them (and potentially their spouse) an income for life.” Michael Martin, a private client manager at Seven Investment Management, agrees. He says: “Annuity rates are low today by historical standards, but when they enable someone to live comfortably [and securely], I would not deem them to be poor value.”

2) I want to maximise income in the first decade of retirement, and then run down my pension pot capital

Running your pension down to nothing during your retirement may appeal to those without children. However, financial planners will often advise that the risks outweigh the rewards of such a strategy, given that no one knows how long they will live. Even with a sizeable pension pot, there no guarantees, as you could live for another 30-40 years after retiring.

“Again, an annuity should be considered,” says Connolly. “It might only pay a small income, but at least you know that income will last for the rest of your life. For those relying just on their personal and state pensions in retirement, running down your pension is a very risky approach.”

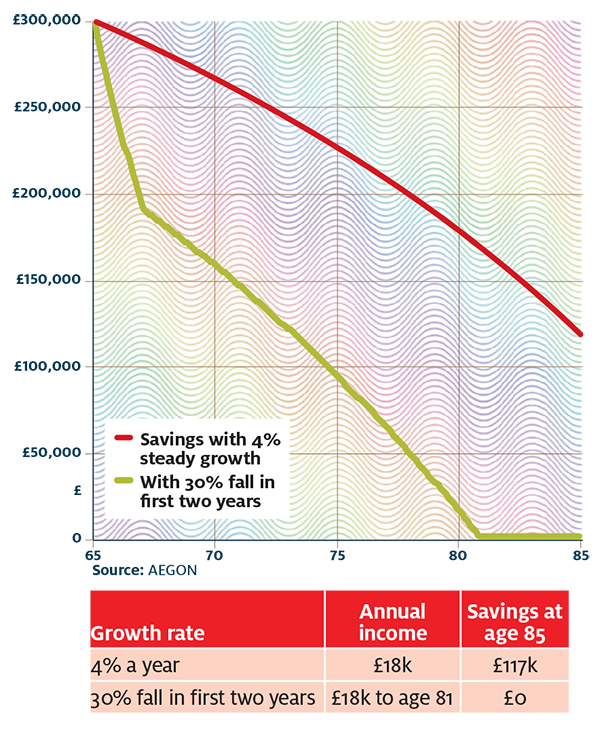

In addition, depleting your pension capital in the first decade of retirement risks opening up a can of worms when stock markets are volatile. Under a scenario where stock markets fall and income withdrawals are maintained or increased during that period, it is difficult for a retirement fund’s capital value to recover afterwards. That’s particularly so if you’re drawing on capital to maintain the required level of income when the market falls (as opposed to taking only ‘natural’ yield in the shape of dividends and interest), as reducing the number of fund units you own makes it much harder for the fund to regain value.

If you continue to draw income from a pension pot at that stage, a vicious cycle is created, resulting in the number of units and value of investments reducing further and potentially running out before you die. The phenomenon is known as pound-cost ravaging – the inverse of pound-cost averaging (see the chart).

Bullard says: “Be aware that the more pension you take upfront, the less you will have for later on. This sounds obvious, but at the beginning of retirement, when your pension pot is at its biggest, the combined impact of dividend and capital growth is at its greatest, and this has compounding benefits. Erode capital too quickly at this point and you can bring forward the point when you run out of cash quite dramatically.”

Ensure withdrawals are made in the most tax-efficient manner. The first 25% of your pension can be taken tax-free. Thereafter, pension withdrawals are taxed at your marginal rate.

Depleting a pension investment early in retirement can have a huge permanent impact on savings

3) I would like to leave a decent legacy to my children and grandchildren

Those aiming to leave a legacy for their children or grandchildren should leave their pensions untouched and, instead, take income from Isas and other investments. This is because, unlike Isas, pension assets aren’t usually subject to inheritance tax. Another attraction is that pension money passed on by those who die before age 75 is tax-free; the beneficiaries of those who die at age 75 or later will pay income tax on withdrawals.

Crucial questions

The question of how to invest a pension pot to be passed on to younger family members boils down to your time horizon. Bullard says: “If your pension is intended to form the basis of your grandchildren’s pensions, you can afford to be adventurous. But if when they inherit your pension pot they are likely to need the cash immediately, you might want to take a more balanced approach.”

A sensible strategy, if you have a long-term time horizon, is to reinvest the income generated from underlying investments held in a pension pot. This will reap the rewards of compounding. Indeed, over the long term, dividend growth is where the vast majority of the stock market’s returns come from.

Those who only have a final salary (defined benefit) pension and would like to leave a pension legacy face a dilemma. While final salary schemes will usually pay out to the spouses of deceased scheme members, typically only half the pot will go to them (and the pension will die with them). However, if a final salary pension is transferred into an investment-based pension, the entire pension can be bequeathed to anyone.

How much retirement income am I going to need?

Financial advisers use cash flow modelling to work out whether a pension investor’s investment portfolio can deliver their desired retirement income.

This involves calculating the likely portfolio growth rate and the amount of retirement income they would like. Both essential and discretionary spending need to be factored in. The state pension, which pays almost £8,800 a year or just shy of £17,500 per couple, is also considered.

Claire Walsh, head of advice strategy at Schroders Personal Wealth, says: Determining the most appropriate pension strategy is a complex process. The first question to ask is: how much do you need to spend each year in retirement? Surveys indicate that a couple can live comfortably on £27,000 a year, but you will need to spend £18,000 a year for the most basic of retirements. For a singleton, the equivalent numbers are £20,000 and £10,000.

“Only once you know the size of your income gap can you determine the return you need to generate. An adviser can help you get a clear understanding of your long-term cash flows. They can then help you determine the return you should aim to generate, given the level of risk you are happy to accept.”

Investment trust picks for ‘annuity proxy’ income in retirement

Investors on the lookout for a long-term investment that produces income at retirement and aims to preserve capital should consider investment trusts over open-ended funds, as they are more reliable income payers. Investment trusts can provide greater income consistency because they can build ‘rainy day’ funds: 15% of the income a trust generates each year can be held in reserve. Open-ended funds can’t do this, because they must return whatever income is generated to investors.

More than 40 investment trusts have increased their dividends for a decade or more. Four trusts that have produced dividend growth for more than 50 years are City of London, Bankers, Alliance Trust and Caledonia Investments.

The problem for investors is that, despite dividend consistency being an attraction, in the majority of cases investment trusts with long dividend growth track records today have relatively low dividend yields, typically around 3%.

Kepler, an investment trust analyst, adopts a different approach when assessing potentially suitable candidates for investors looking for alternatives to an annuity. It has a list of “annuity income picks” aimed at investors who prioritise yield above all. A spokesperson explains: “While we hope to at least maintain capital values in inflation-adjusted terms, we are willing to accept the risk of a slow erosion of capital, if necessary.”

The 2020 line-up is shown in the accompanying table.

Kepler’s annuity income trust picks

| Trust | Yield (%) |

|---|---|

| Real Estate Credit Investments | 7.1 |

| Invesco Enhanced Income | 6.5 |

| HICL Infrastructure | 6.1 |

| Tetragon | 6.0 |

| TwentyFour Income | 5.7 |

| Greencoat UK Wind | 5.0 |

| Hipgnosis | 4.7 |

| Henderson Diversified Income | 4.7 |

Source: Kepler and Winterflood, as at 3 February 2020.

In the April issue of Money Observer magazine, we will examine the investment trusts chosen by Kepler in more detail. We will also take a look at other open-ended funds and investment trusts worth considering as annuity proxies. Subscribe to Money Observer here.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.