Did defensive funds protect investors during the market sell-off?

From investment trusts and gold, to absolute return funds and ‘volatility managed’ funds, Kyle Cald…

2nd April 2020 10:39

by Kyle Caldwell from interactive investor

Share on

From investment trusts and gold, to absolute return funds and ‘volatility managed’ funds, Kyle Caldwell examines the performance of defensives during a turbulent time.

Those outright pessimists who long warned a financial apocalypse was around the corner during the 10-year long bull market for financial markets had concerns over unsustainably high levels of global debt, trade wars and sky-high valuations for the US equity market. Each worry was plausible, but ultimately none of them proved to be the straw that broke the camel’s back. Instead it was Covid-19, a deadly disease no one had heard of until the start of this year, which sent markets into meltdown.

At such times, defensively positioned funds should, in theory, prove their worth and cushion investors by limiting losses. After all this is the role they are designed to perform in a portfolio, and indeed the reason why investors willingly accept the trade-off of lagging returns in a rising market.

But, research by Money Observer has found a number of defensive funds did not in fact prove their worth during the sell-off. Using data from FE Analytics, covering the period from 21 February (when the sell-off started) to 23 March (prior to US and Asian markets having their best three-day streak since the 1930s), we examine how different types of defensive funds fared.

- What does coronavirus mean for your retirement plans?

- Coronavirus forces UK banks to freeze their dividend payments

Capital preservation-focused investment trusts

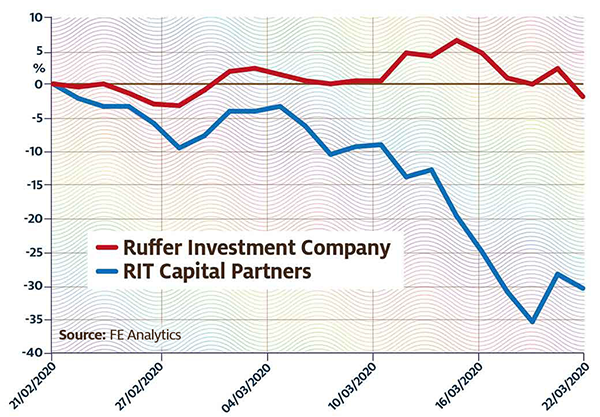

There are a handful of wealth preservation investment trusts, which prioritise protecting investor capital and invest on the principle that they would sooner keep £1 rather than risk losing it to try and win £2. The four trusts that meet this description are Capital Gearing, RIT Capital Partners, Ruffer Investment Company and Personal Assets. Each has a low weighting to equities and plenty of defensive armoury, such as low-risk inflation-linked bonds and a small weighting to gold.

But over the period of the sell-off, performances markedly varied. Ruffer held up best (with its share price total return down 1.9%), while Personal Assets (-11.2%) and Capital Gearing (-11.8%) produced similar losses.

RIT Capital Partners, meanwhile, posted a heavy loss of 30.5%, which was steeper than global tracker funds. Over the same period, the FTSE World index return was -24.7%. This is far from the steady ride its shareholders expect, but can be explained by the fact that it moved from trading on a small premium (of 4.3% on 21 February) to a 20% discount (on 23 March), according to data from investment trust analyst Winterflood. Over that period there was clear selling pressure, therefore, which harmed its share price. However, it should be pointed out that this abnormally wide discount did not last for long, as a week later (30 March) its discount fell to -9% and its share price rose by 20%.

James Carthew, head of investment company research at QuotedData, says the fact that RIT Capital Partners only publishes its net asset value once a month “created some uncertainty”. But he thinks the sell-off has been unjustified. “In addition to the net asset value issue, a large part of the portfolio is invested in hedge funds and unquoted investments and the value of these is less visible. Providing its net asset value holds up well, we see no reason why the discount should not close.”

The other three wealth preservation trusts have not been under selling pressure. Over the period Ruffer’s small discount tightened towards par, while both Personal Assets and Capital Gearing saw their small premiums slightly increase.

Peter Spiller, manager of the Capital Gearing investment trust, which has a very low allocation to equities (17% at the end of February), is continuing to adopt a cautious stance. He says: “A big constraint on buying (despite the sell-off) is that the S&P 500 is expensive. If Wall Street goes down, then so will global markets.” As such, Spiller argues, value is not yet compelling.

Two trusts compared

Low-risk multi-asset and ‘volatility managed’ funds

In theory, multi-asset funds, owing to their greater levels of diversification, should be better equipped to weather a market storm than equity funds that either invest globally or focus on a particular region.

This rang true: over the timeframe in question, the Investment Association (IA) 0-35% equities share sector showed an average fund loss of ‘just’ 12%. As expected, other multi-asset sectors that carry greater levels of risk produced bigger losses. The IA 20-60% equities share sector was down 17.5%, while the IA 40-85% equities share sector showed an average fund decline of 21.2% – slightly worse than the IA flexible sector, with an average decline of 20.9%. To put these losses into some context, the IA global sector declined by 24.1% and the IA UK All Companies sector posted an average loss of 35.9%.

The volatility managed fund sector disappointed, though, with the average fund in the sector declining by 18%. In November, this was the top-selling IA sector, drawing in conservative investors as such funds target a specific risk or volatility outcome.

Darius McDermott, managing director of FundCalibre, the fund ratings provider, points out that the losses incurred serves as a warning: “The sector is volatility-managed - not volatility-free.”

He adds: "I think the volatility managed sector hasn't done as well because it tends to be dominated by funds which invest via passives. We have actually seen many active funds hold up better than passives in this environment. A lot of these funds just seem to be filled with 10 tracker funds, which hasn't worked as it has been an environment where diversification and correlations haven't meant much because everything has gone down together, albeit a diversified portfolio has obviously gone down less than equities alone.”

Absolute return funds

The reputation of absolute return funds has taken a battering over the past couple of years, but during the past month’s heavy market sell-off the majority of funds in the sector have proved their worth. Over the period, the average fund in the sector posted a loss of 8.8%. Overall, one third of absolute return funds managed to limit losses to less than 5%, and in the case of six funds gains were made. Another one-third of the sector lost between 5% and 10%, while the remaining one-third posted losses in excess of 10%.

Nonetheless, at the bottom of the table steep losses were made: Polar Capital UK Absolute Equity (-36.7%), Natixis H2O MultiReturns (-35.8%) and GAM Star Global Rates (-28.7%) were the bottom three performers.

Fund managers running absolute return funds have a plethora of tools at their disposal to try and protect investors’ capital during more turbulent times. These include the ability to go short – betting against the fortunes of a company in order to make money if its share price falls.

The trouble is that when the wrong calls are made, losses are magnified, which investors in many of these funds found to their cost over the years during other notable market sell-offs. This time around, though, so far at least, most have done their job in protecting capital and reducing risk for investors by fulfilling their role as diversifier in a portfolio.

McDermott points out that global macro funds have generally held up well, including Allianz Fixed Income Macro (up 4%), JPM Global Macro (-1.4%) and Invesco Global Targeted Returns (-2.3%). He also notes that absolute return funds with a long/short equity approach have also generally been resilient: Janus Henderson UK Absolute Return(-3.4%), Smith & Williamson Enterprise (-8.4%) and BlackRock UK Absolute Alpha (-8.1%).

How ‘safe-haven’ gold fared

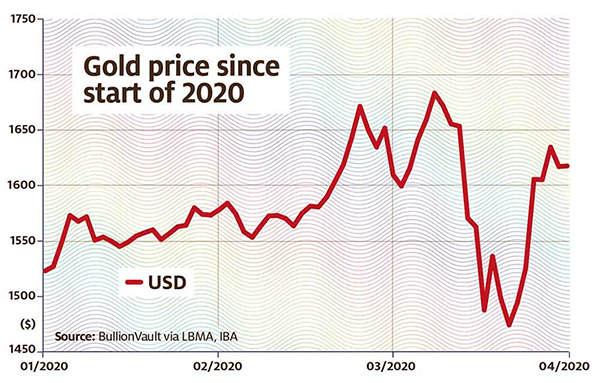

Gold is widely viewed as a safe-haven investment that protects capital during market downturns, but over much of the market sell-off it failed to perform this role. The gold price declined around 10% from 24 February to 16 March, the period that saw the steepest falls for global markets.

Various commentators attribute the fall to gold getting caught up in a rush for liquidity (and gold is liquid and easy to sell) across all asset classes in order to raise cash. In the months ahead, though, various commentators expect the gold price to return to form following the intervention of governments and central banks to “do whatever it takes” through enormous monetary and fiscal stimulus packages. Governments and central banks cannot print more gold, as they can currencies. As a result, its value is retained. In theory, this attribute of the yellow metal will continue to be highly prized by investors, particularly in uncertain times.

John Chatfeild-Roberts, head of strategy for independent funds at Jupiter, has been increasing exposure to gold. He notes: “We still see gold as an insurance policy, but think interventions by governments to keep economies on track will have an effect in that there’s more money flying around, and that will underpin the gold price and probably increases the demand for gold and the price of it going forward.”

The performance of gold since the start of the year

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.