Value trap or too cheap to ignore? The 10 cheapest shares on the FTSE 100 revealed

The blue chip index is currently on a price to earnings (p/e) ratio of 12.5 times with a dividend yield …

20th March 2019 10:16

by Tom Bailey from interactive investor

Share on

The blue chip index is currently on a price to earnings (p/e) ratio of 12.5 times with a dividend yield of 4.7%.

It is no secret that UK companies are currently trading at historically cheap levels. Indeed, as one fund manager has pointed out, the last time UK listed shares were as cheap as they are now (measured in comparison to bonds), Britain was fighting in the First World War.

When it comes to the FTSE 100 in particular, valuations are also attractive. The blue chip index is currently on a price to earnings (p/e) ratio of 12.5 times with a dividend yield of 4.7%. This, says Russ Mould, investment director at AJ Bell, makes the index cheap “both in absolute terms and also relative to the other geographic options available to equity investors.”

He adds: “Such relatively lowly multiples could suggest that a lot of bad news is already in the price, especially after the second-half slump in the index last year.

- Invest with ii: Top UK Shares | Share Prices Today | Open a Trading Account

“After a marked period of underperformance which stretches back to the summer 2016 referendum vote on EU membership, UK equities look unloved and may therefore be undervalued.”

A large number of constituents in the index are even cheaper. There are now 25 FTSE 100 members trading on a p/e ratio below 10. A p/e ratio between 15 and 20 is considered normal.

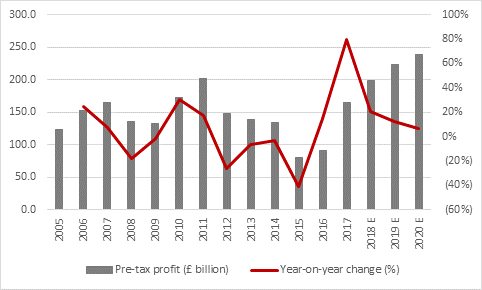

According to Mould, the fortunes of companies in the index are looking up. He points out that analysts are expecting the FTSE 100 to generate an all-time high pre-tax profit of £223 billion in 2019. A number of the cheapest shares also have strong forecasted earnings growth.

He adds: “With 25 FTSE 100 members trading on less than 10 times forward earnings, it is tempting to think that the gloom may just be a little overdone and that even meeting, let alone beating, earnings forecasts could be enough to convince the doubters to return to UK stocks.”

However, while record profits should warm sentiment towards the index, investors should be cautious. Analyst expectations, in theory, should already be baked into the price of FTSE 100 equities. That may result in limited upside should companies simply meet expectations. At the same time, it leaves the risk that actual figures fall short of expectations, the companies will have further to fall.

- Is value investing a broken model?

Moreover, the big Brexit cloud, which has been hovering over the UK market for some time, has not gone away, and the most likely scenario of Brexit being delayed will cause further uncertainty that will continue to unnerve investors.

While the p/e ratio is a useful metric, it should not be used in isolation as an indication of value. Other measures should be used, including price to book value, which is the estimated value of a firm’s assets if it were wound up. Assessing the amount of cash a business is generating is also important, particularly if the share in question is committed to paying a dividend.

| 2019 E | 2019 E | ||

|---|---|---|---|

| Price/earnings ratio | Forecast earnings growth | ||

| 1 | International Cons. Airlines | 5.3 x | 9.4% |

| 2 | Aviva | 6.8 x | 7.8% |

| 3 | TUI AG | 7.3 x | (1.9%) |

| 4 | Barclays | 7.4 x | 0.2% |

| 5 | 3i | 7.6 x | 2.6% |

| 6 | Evraz | 7.7 x | (37.0%) |

| 7 | Persimmon | 7.9 x | 0.3% |

| 8 | BT | 8.4 x | (3.1%) |

| 9 | Lloyds | 8.4 x | 35.6% |

| 10 | WPP | 8.4 x | (5.9%) |

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.